Answer: Blockchain is a decentralized, digital ledger system that securely records transactions and data across a network of computers. It eliminates the need for a central authority, offering transparency, security, and trust in various applications—from finance to supply chain management and beyond. In essence, blockchain and blockchain technology use cryptographic techniques to ensure data integrity, making it nearly impossible to alter historical records. This article explores what blockchain is, how blockchain works step by step, and why it holds transformative potential in fields like security, finance, and beyond.

What Is Blockchain? (Definition and Overview)

Blockchain is often defined as a distributed ledger technology that stores information in groups called blocks. Each block contains a batch of data—commonly transaction details, a timestamp, and a cryptographic reference (hash) linking it to the previous block. This chain of blocks, connected via cryptographic hashes, results in data that is inherently difficult to tamper with. According to TechTarget, the beauty of blockchain technology lies in its ability to provide a transparent and secure record of data or transactions without requiring a central authority.

Key Points:

- Decentralized: Instead of a single server or authority, the network is maintained by multiple nodes.

- Immutable: Each new block references the hash of the previous one, making alterations exceedingly difficult.

- Consensus: Nodes must agree on the validity of each transaction before it is stored on the chain, enhancing trust.

Blockchain technology gained worldwide attention with the advent of Bitcoin in 2008, but its potential extends well beyond cryptocurrencies. From supply chain tracking to legal contracts and digital identity management, blockchain’s versatility continues to spur innovation.

Who Invented Blockchain?

While research into cryptographically secured chains of blocks preceded Bitcoin, the blockchain concept as implemented in Bitcoin is credited to the pseudonymous person (or group) known as Satoshi Nakamoto. Nakamoto introduced blockchain technology in a 2008 whitepaper titled Bitcoin: A Peer-to-Peer Electronic Cash System. Though Bitcoin and blockchain were initially synonymous to many, they are distinct: Bitcoin is a cryptocurrency that uses blockchain as its underlying data structure. Over time, other innovative projects have adapted blockchain’s principles to solve real-world problems beyond cryptocurrency.

Developers and researchers have built upon Nakamoto’s framework by introducing new consensus mechanisms, privacy features, and scalability solutions. Hence, while Satoshi Nakamoto remains the credited inventor, ongoing contributions from a global community of developers and academics continue to refine and expand the technology.

How Blockchain Works Step by Step

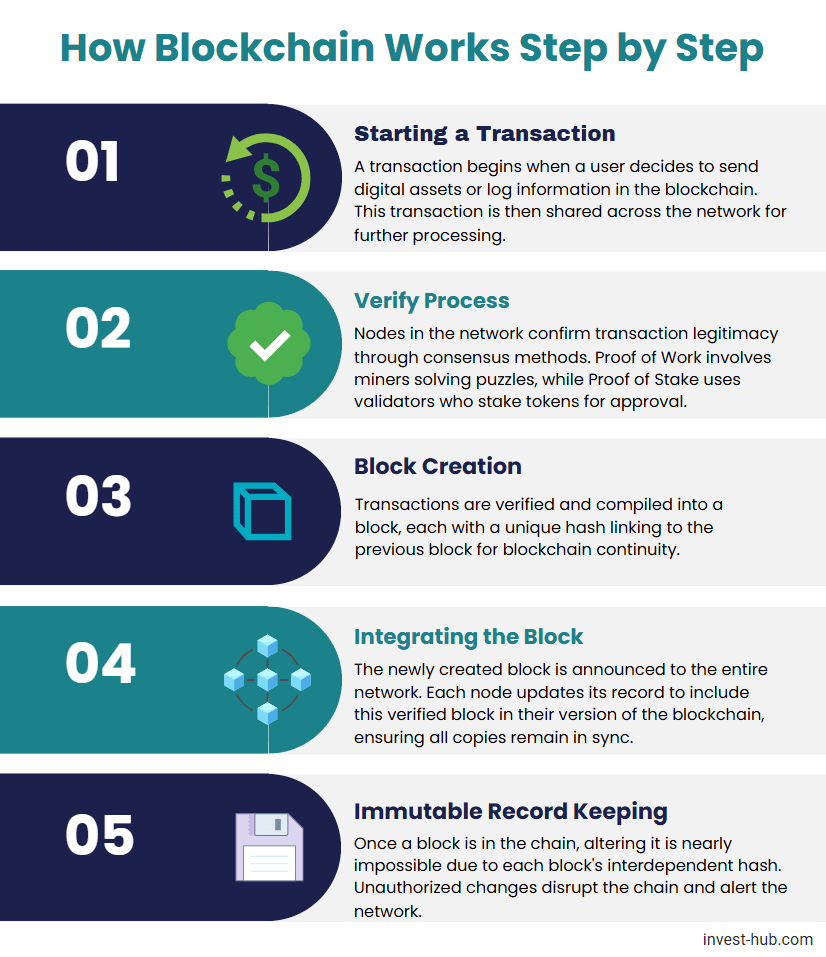

Understanding how blockchain works step by step can help demystify this groundbreaking technology. Below is a simplified sequence of events that illustrates the typical flow of data or transactions within a blockchain network:

- Initiation of a Transaction

- A user initiates a transaction (e.g., sending digital currency or recording supply chain data).

- This transaction is broadcast to the network.

- Validation and Verification

- Multiple nodes on the network validate the transaction using a consensus mechanism (e.g., proof of work, proof of stake).

- In Proof of Work, miners compete to solve cryptographic puzzles; in Proof of Stake, validators stake tokens to confirm transactions.

- Creation of a Block

- Once the network verifies transactions, they are bundled into a new block.

- The block includes a reference (hash) to the previous block, maintaining the chain’s continuity.

- Block Addition to the Chain

- The new block is broadcast to all nodes.

- Nodes update their ledgers, adding the verified block to the chain.

- Permanent Record

- Once added, blocks cannot be easily altered because each block’s hash depends on the data within it and the previous block’s hash.

- Any tampering would break the cryptographic link, instantly alerting the network to a discrepancy.

This structure ensures data consistency across the entire network, removing the need for a single, central gatekeeper. The blockchain technology model builds trust through a transparent, verifiable process.

Key Characteristics of Blockchain

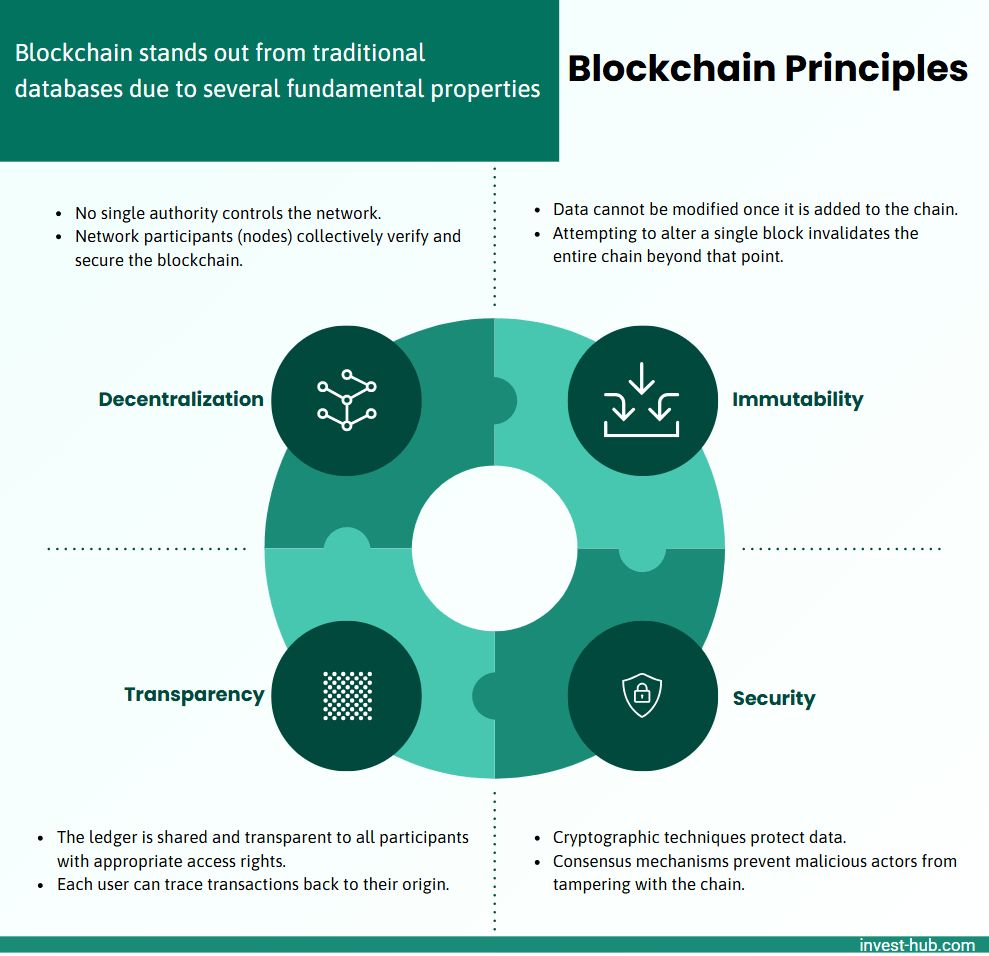

Blockchain stands out from traditional databases due to several fundamental properties:

- Decentralization:

- No single authority controls the network.

- Network participants (nodes) collectively verify and secure the blockchain.

- Immutability:

- Data cannot be modified once it is added to the chain.

- Attempting to alter a single block invalidates the entire chain beyond that point.

- Transparency:

- The ledger is shared and transparent to all participants with appropriate access rights.

- Each user can trace transactions back to their origin.

- Security:

- Cryptographic techniques protect data.

- Consensus mechanisms prevent malicious actors from tampering with the chain.

As AWS notes, these characteristics are integral to why blockchain is important: by providing trust in environments where participants may not fully know or trust each other.

Types of Blockchain

As blockchain technology evolves, several distinct types of blockchain have emerged, each tailored to different requirements and use cases:

| Type of Blockchain | Characteristics | Typical Use Cases |

|---|---|---|

| Public Blockchain | – Completely open and decentralized – Anyone can join and participate in the network – Commonly used for cryptocurrencies (e.g., Bitcoin, Ethereum) – High transparency but can be slower or more resource-intensive | – Cryptocurrencies – Open-source projects |

| Private Blockchain | – Operated by a single organization or a select group of parties – Access is restricted – Only approved participants can validate and add new blocks – Offers better control, privacy, and efficiency | – Enterprise solutions – Internal data management |

| Consortium (Federated) Blockchain | – Governed by a group of organizations rather than a single entity – Partially decentralized – Preserves some efficiencies of a private chain – Ideal for industry-wide collaborations | – Banking consortia – Collaborative supply chains |

| Hybrid Blockchain | – Combines elements of both public and private blockchains – Some data is publicly accessible, while sensitive information remains private – Offers customizable transparency and control | – Supply chain management – Finance (selective privacy) |

Each type of blockchain serves specific organizational or community needs. Public chains emphasize transparency and decentralization, whereas private and consortium networks focus on efficiency, governance, and selective data sharing.

Are Blockchain and Cryptocurrencies the Same?

A common misconception is that blockchain and cryptocurrencies like Bitcoin or Ethereum are interchangeable. In reality, are blockchain and cryptocurrencies the same? The short answer is no. While most cryptocurrencies use blockchain technology as their underlying infrastructure, blockchain itself is a broader concept applied in many other contexts:

- Cryptocurrencies: Digital tokens, such as Bitcoin or Ether, transferred on a blockchain network.

- Smart Contracts: Self-executing contracts with terms directly written into code, used in supply chain or real estate.

- Identity Management: Systems that provide secure, verifiable digital identities.

- Tokenization of Assets: Representing real-world assets (like art or property) as tokens on a blockchain.

Different projects utilize various consensus algorithms and programming environments, yet all share the fundamental structure of blockchain. Cryptocurrencies are one of many possible use cases for blockchain technology but do not encapsulate all of its applications.

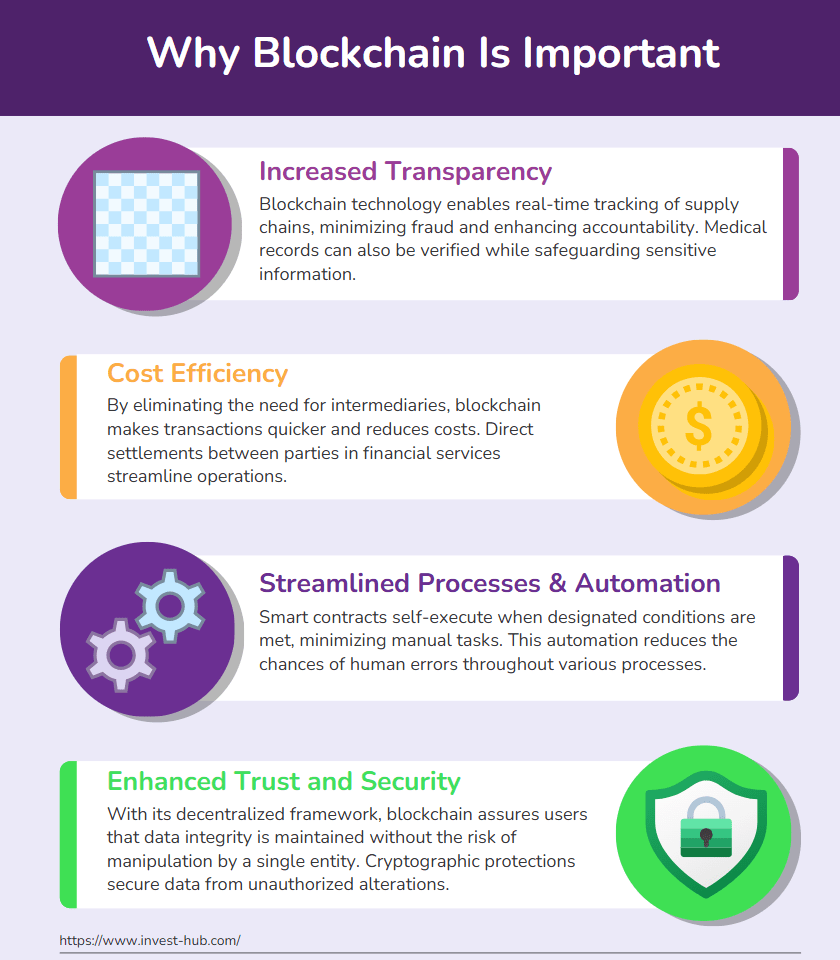

Why Blockchain Is Important

Organizations worldwide are exploring blockchain due to its potential to transform traditional operations. Some key reasons why blockchain is important include:

- Enhanced Transparency

- Supply chains can be tracked in real-time, reducing fraud and improving accountability.

- Medical records can be verified without exposing private data.

- Cost Reduction

- By removing intermediaries, transactions can become faster and cheaper.

- Banking and financial operations can settle directly between parties.

- Improved Efficiency and Automation

- Smart contracts automatically execute once certain conditions are met, reducing manual paperwork.

- Processes become less prone to human error.

- Trust and Security

- A decentralized structure assures users that no single entity can alter the records.

- Cryptographic safeguards defend data against unauthorized changes.

These features push blockchain technology to the forefront of digital transformation strategies in finance, healthcare, governance, and more.

Common Use Cases of Blockchain Technology

Blockchain technology offers flexibility across diverse industries. Here are a few prominent use cases, along with real-world examples:

1. Financial Services

- Cross-Border Payments: Reduced transaction times from days to seconds or minutes.

- Decentralized Finance (DeFi): Platforms enabling peer-to-peer lending, yield farming, and other financial products without a central entity.

- Example: Ripple, Ethereum-based DeFi projects.

2. Supply Chain Management

- Product Tracing: Track items from origin to store shelves to ensure authenticity.

- Quality Control: Automatic triggers if goods deviate from temperature requirements or quality standards.

- Example: Walmart and IBM’s Food Trust platform.

3. Healthcare

- Electronic Health Records (EHR): Easily shareable and tamper-proof patient data across hospitals.

- Clinical Trials: Immutable data records for transparency in drug development.

- Example: MedRec, a blockchain-based EHR system.

4. Government and Public Services

- Voting Systems: Tamper-proof digital ballots to reduce election fraud.

- Land Registries: Transparent records of property ownership.

- Example: Several pilot projects in countries like Estonia and Georgia.

5. Intellectual Property Management

- Patents and Copyrights: Immutable timestamps for creative works.

- Example: Blockchain-based music platforms that distribute royalties automatically.

According to TechTarget, these use cases underscore the wide-ranging benefits of blockchain’s distributed ledger system.

Blockchain for Security: Enhanced Protection and Reliability

Security stands at the heart of blockchain. By design, the network’s decentralized nature guards against single points of failure. This structure, combined with cryptographic algorithms, provides layers of defense. Below are ways blockchain for security amplifies protection:

- Distributed Consensus

- No central server to hack.

- Attackers would need to gain control over a majority of nodes—often an extremely expensive or near-impossible task in large public blockchains.

- Immutable Ledger

- Data, once verified and added, is permanently recorded.

- Attempting to change a record in one node’s copy triggers discrepancies across other nodes.

- Private and Permissioned Chains

- Organizations can implement blockchain technology with controlled access, where only authorized parties can participate.

- Enterprise-level security measures (e.g., hardware security modules) can layer on top of the blockchain system.

- Reduced Fraud and Counterfeiting

- Real-time audits and traceability mitigate deception in supply chains and financial sectors.

- Any anomalies are quickly detected as the network automatically validates each transaction.

Still, blockchain does not guarantee absolute security; it must integrate with secure endpoints, robust smart contract code, and vigilant governance models. A holistic security approach is necessary to realize the full potential of distributed ledgers.

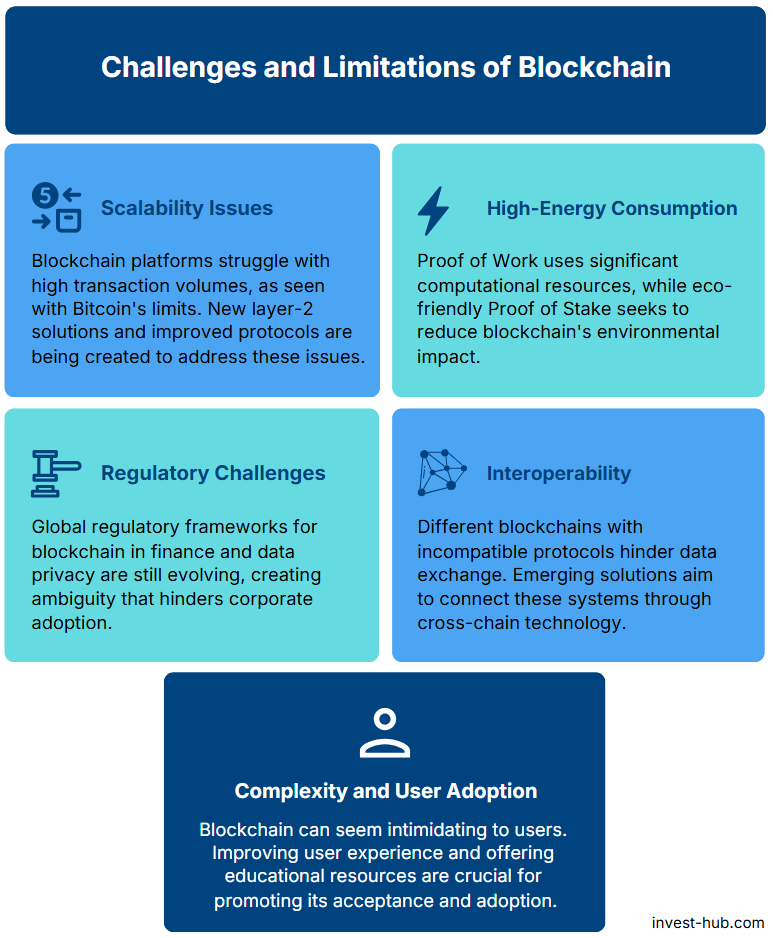

Challenges and Limitations of Blockchain

Despite its promise, blockchain faces several hurdles:

- Scalability

- Some blockchain networks struggle to process large volumes of transactions quickly (e.g., Bitcoin’s throughput limit).

- Layer-2 solutions and newer protocols aim to address these concerns.

- Energy Consumption

- Certain consensus algorithms (proof of work) require significant computational power.

- Ecologically conscious alternatives like Proof of Stake attempt to reduce environmental impact.

- Regulatory Uncertainty

- Governments worldwide are still formulating laws for blockchain usage, especially for financial transactions and data privacy.

- Unclear regulations can hinder corporate adoption.

- Interoperability

- Different blockchains often use incompatible protocols, making data exchange difficult.

- Cross-chain solutions and protocols aim to bridge these gaps.

- Complexity and User Adoption

- Many end-users find blockchain technology confusing.

- A smoother user experience and clearer educational resources are needed for widespread adoption.

These issues underscore that blockchain is not a one-size-fits-all solution. Each use case must evaluate whether its benefits outweigh these limitations. Organizations must assess integration costs and compliance requirements before implementing blockchain-based solutions.

Future Outlook of Blockchain Technology

The future of blockchain technology is filled with both excitement and uncertainty:

- Scalable Protocols

- Newer blockchains (e.g., Solana, Avalanche) offer higher throughput.

- Layer-2 solutions like Lightning Network (Bitcoin) or Optimism (Ethereum) aim to reduce network congestion.

- Enterprise Adoption

- Major corporations experiment with private and hybrid blockchains for internal process optimization.

- Financial institutions investigate central bank digital currencies (CBDCs).

- Regulatory Frameworks

- Governments are gradually clarifying regulations around cryptocurrencies, ICOs (Initial Coin Offerings), and data management on distributed ledgers.

- More robust legal frameworks could boost mainstream adoption.

- Integration with Emerging Technologies

- Combining blockchain with IoT devices can enhance traceability and automation.

- AI-driven smart contracts might increase efficiency and adaptability in business workflows.

- User-Friendly Applications

- Startups focus on simpler wallets, decentralized applications (dApps), and intuitive interfaces.

- Wider acceptance is likely if the user experience becomes as seamless as using traditional web or mobile apps.

As the technology matures, experts from IBM and other leading organizations predict that blockchain’s role will expand significantly in finance, governance, and beyond.

Conclusion

In today’s rapidly evolving digital landscape, blockchain stands as a powerful solution for secure, transparent, and decentralized record-keeping. By understanding what blockchain is, how blockchain works step by step, and the various applications where blockchain technology can be implemented, both businesses and individuals can recognize its transformative potential. While challenges around scalability, regulation, and user adoption remain, ongoing innovation and growing acceptance indicate that blockchain is here to stay.

As the technology continues to advance, now is the ideal time to explore blockchain’s capabilities—whether through building new applications, learning the technical foundations, or simply staying informed about the latest developments.

Frequently Asked Questions (FAQ)

Blockchain is a distributed ledger that securely records data in linked blocks. Each new block references the previous one, making the chain of records nearly impossible to alter. It operates without central authority, relying on a network of nodes to verify transactions.

Unlike a centralized database where a single entity controls the system, blockchain distributes data across multiple nodes. Modifying a record requires changing it on all nodes, making blockchain technology inherently more secure and transparent.

No. While cryptocurrencies like Bitcoin and Ethereum use blockchain as their underlying technology, blockchain itself can be applied in many other areas such as supply chain, healthcare, and digital identity management.

Satoshi Nakamoto, a pseudonymous person or group, introduced blockchain technology in the 2008 Bitcoin whitepaper. Though research on cryptographically secured ledgers predates Nakamoto, Bitcoin popularized the modern concept.

Blockchain for security relies on decentralization and cryptographic hashing, preventing a single point of failure or data tampering. Each block depends on the previous block’s hash, making unauthorized modifications extremely difficult.

You can refer to reputable sources like IBM, Invest-Hub, AWS, and university courses. Hands-on tutorials for popular blockchain platforms (e.g., Ethereum) also provide practical experience.